Appreciate the proposal. I’m not opposed to reducing inflation, but I’m starting to think these short term bandaids are not going to help. People want stability. Not in price, in the protocol. (Ironic since the price is more stable than the protocol at this point in time). All these protocol changes disrupt the confidence and mess with the economics behind what this network is trying to achieve.

To @adam 's point, WAGMI didn’t work to the extent it was meant to. Node count has only dropped 30% from peak, while price dropped over 90%, and my sense is most of the unstakes are just waiting on the sidelines to restake after PIP-22. So inflation will absolutely need to be addressed for sure, but piling on more changes in the midst of PIP-22 and light-client is compounding uncertainties. We need a new baseline after these changes to operate from and assess properly with data.

I think we should slow our roll a bit, see the effects of the changes that have already been passed, and then assess what changes need to be made. With that being the case, extending WAGMI doesn’t make sense at this point in time.

I think it is premature to move this to voting I do not think this has been properly vetted. I have not seen adequately addressed the concerns raised by @TheDoc and @CryptoEdge@sztanyel and @adam though I do acknowledge and appreciate the counter-arguments presented by @o_rourke and @cryptocorn. Nor have seem any analysis that indicates that further gradual reduction is superior to both “do nothing” (e.g., keep pokt supply growth at 50%) and “immediate jump” to final desired state (e.g., immediate jump to WAGMI Targe supply growth = 20%)

First action of this proposal would take place around Aug 21. Subtracting 1 week for voting, I believe that allowing discussion and analysis to contiue for the next two weeks would be prudent and have no effect on the implementation timeline. In the original self-comment to the proposal, @cryptocorn stated, "I look to collaborate with the community and in particular invite @adam and @msa6867 to review the proposal and tokenomics effects the proposal will have. @adam reviewed and gave comment above that he feels waiting for the dust to settle from PIP-22/PUP-21 and LC is prudent before taking on other economic changes. I had indicated that my work flow would not allow me to give adequate attention to this proposal until starting this week after PUP-21 was complete and I thought I had secured assurance that this timeline was acceptable. So it was with some consternation that I sawPUP-22 was moved to voting at essentially the same time as PUP-21.

It is important to note that final state is heavily influenced by the road taken to get there. In the case of PUP-21, when faced with some uncertainties regarding system behavior in the face of raising the cap (multipier effect), we floated the idea of going up to 4x incrementally… e.g., 2x then 3x then 4x, allowing to study system response at each step beforeoving up to next step. The problem with taking that more gradual approach and the reason we rejected it is that it may have disincentived meaningful node-count reduction via consolidation compared to jumping straight to 4x. The same effect needs to be taken into consideration here. I think @adam point above is that if in February we had jumped straight to the final WAGMI=50% state, it may have triggered a substantial exodus of “retail” node runners resulting in reduced node count and therefore reduced sell pressure from covering infra cost as compared to the slow-cook method that was adopted. He further asks (essentially), if original PUP-11/13 did not result in a reduction in node count (and thus reduction in infra costs), what makes us think that more of the same will. Therefore I must respectfully disagree with @JackALaing when he says, “With these points in mind, knowing the options that will continue to be available to us, we shouldn’t let a disagreement about the reduction timeline get in the way of incremental progress.” If debate is needed as to whether the “shock-and awe” of a BIG reduction jump in reward is what is needed to get inefficient node runners to “shape up or ship out” then making “incremental progress” will make it progressively harder and evenually impossible to implement a “shock-and’awe” response if that turns out to be the consensus best choice. Much better it would seem to do nothing for the moment than to rush into a vote that we aren’t ready for.

Counterexample: pancake swap. A serious project with real revenue and profitability roadmap, at about the same level of maturity as Pocket network, nearing the completion of its second year. Running at about 80% anual growth in token supply. And suffering no discernable negative effect from that supply growth in comparison to similar non-“inflationary” projects. (NFI!) The problem with pocket has never been about growth in token supply per se, but always about the proliferation of high-cost, under-utilized nodes well beyond the system needs leading to unrelenting sell pressure to cover infra costs.

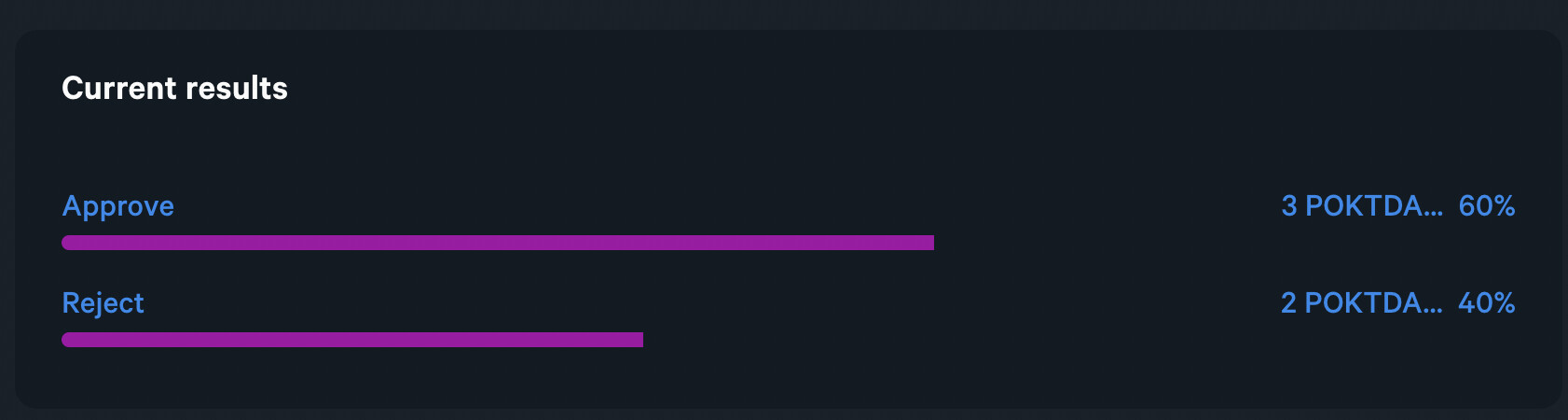

Cryptocorn has asked me to cancel the vote so that more discussion can be had as msa outlined and Cryptocorn had intended. This was a misunderstanding on my part.

This was the result at the time of the vote being cancelled:

A) Further inflation reduction or ABR or Both

B) Timing, Now, Gradually (Like WAGMI) or Q4

One thing that seems more certain is that the relays are growing at a steady rate and more chains are being added, this will in turn increase the $POKT created.

What is uncertain is the effect of the Weighted Staking on the number of Node Runners and how they consolidate.

I would suggest to get see the results (or as much as possible) of the new weighted staking, see how the node runners have reacted and then adapt to that, essentially make a decision with more ‘actual ‘ data, rather than speculation, this does of corse rely on the update being pushed live in time in August so Node runners can have time to decide on their strategy.

Disclosure: Im a node runner via Easy2Stake, that has already decided my play and am in the second 21 day unstaking period, I’m also an investor in Crypto, Deep Tech, Fintech and AdTech.

intent to agree but inflation at 50% just surreal I mean for you nodders maybe and for project itself with current inflation POKT going no were and we will struggle

fully support this proposal and yes 20% inflation still high and you got guys who wants to keep current inflation, this just shows how nerds these folks are, not excited for the project but just for their beneficial.

Reduce to 20% immediately or like suggested in the proposal. Implement ABR and Reduce further next year at the latest. I think all the arguments have been brought up before. Every day of 50 pct inflation is suicide

at the current stage I admire we would need 50 pct inflation at current stage with got to reduce it and from there we can increase it when there is demand

What’s the reasoning behind this choice? Why have the increase be compounding for the remainder of 2022 then linear from 2023 onwards? You’re just creating more inflation in 2022.

Edit to add:

The original WAGMI did not re-baseline, we always worked from the original supply snapshotted at the time of the WAGMI proposal passing. As such, re-baselining for the September 1st change to a 35% target actually increases inflation relative to the current 50% target (which is anchored against the original supply).

Different RelaysToTokensMultiplier values, assuming 30-day trailing avg relays of 944.5M (which was used for the latest 50% adjustment that resulted in a RTTM value of 1371):

Targeting 35% using original supply of ~945M: 959

Re-baselining to target 35% using current supply of ~1.36B: 1381

If we opt to re-baseline, the next WAGMI “reduction” will increase RTTM from 1371 to 1381 (avg relays held equal). If we opt to continue using the original supply at the time of WAGMI passing, the next WAGMI reduction will decrease RTTM from 1371 to 959 (avg relays held equal), which corresponds with what we would expect to happen reducing from 50 → 35 (1371*(35/50)=959.7).

The following thoughts are my own and do not necessarily represent the viewpoints of @cryptocorn or @adam.

The reasoning was to bring clarity. and transparency. and fix an ambiguity in the original WAGMI proposal that has led to an incorrect perception of present inflation rate. The original PUP-13 was ambiguous in regard to baseline. Upon rereading PUP-13 I discovered that you had inserted a comment on Feb 28 stating that it was the intention of the Foundation to baseline POKT supply as of the time of PUP-13 passing and hold it constant for the duration of the PUP-13 changes. That brought the necessary clarity to resolve the ambiguity but frankly such clarity needs to be in the body of a proposal and not buried in the comments section. I confess that I missed that nuance and have been operating under a different assumption. In the same spirit of your comment of Feb 28 in which baseline was naturally set to the value at the time of passing the proposal, a baseline would naturally be reset at the time of the passing of a follow-on proposal.

Right now, according to how the Foundation has interpreted PUP-13, the actual annualized inflation rate for POKT sits at just under 35%, not at 50%. If no follow on action is taken to PUP-13, then the inflation rate in subsequent years will be as follows (even less to negative when ABR turns on):

2023: 31.1%

2024: 23.7%

2025: 19.2%

All of this ought to have been spelled out explicitly in the original WAGMI proposals. While it may have made no difference in the actual tokenomics (the same number of tokens are minted no matter what you call the “inflation” rate), this makes a large difference in the outside world where “perception is reality”. How many potential investors were scared off by the “50%” inflation rate for Pocket that gets repeated as a mantra. That misperception alone may have cost downward pressure on the market valuation of POKT leading to higher percentage of node runner rewards being sold to cover infra costs. All because of a misperception!

That being said, it is not our intention to go backwards on TMMR values. we will either reduce the entire set of 35-29-24-20 numbers downward to reflect the re-baselining, or else we will reformulate the construct to be one of setting a target average monthly mint rate rather than a target “inflation”, since this, at its core, is what the original WAGMI always was according to how it has been interpreted.

Where does this assertion come from? If you’re annualizing the inflation rate from the date of the proposal passing, then the inflation rate actually sits somewhere above 50%, since we’ve gradually worked our way down monthly to 50% from 100%.

If the standard practice when we talk about annualized inflation rate is to calculate it from today’s date, then I’m not opposed to us updating to follow that practice, but then why does PUP-22 switch to a fixed baseline as of Jan 1st 2023? Does that not suggest that PUP-22’s definition of target “inflation” is also inconsistent?

You’ve alluded to this in your response but I would suggest either of two paths forward:

Define target inflation as an annualized metric anchored around a fixed baseline from the beginning of each year. Feb 28th for the original WAGMI, since that’s when the proposal passed, Jan 1st 2023 when we get to the 20% target. Keep the target numbers as they are.

Update target inflation to mean from the date of the RTTM value being updated. Continue re-baselining every time we update the parameter, including from Jan 2023 onwards. Reduce the entire set of numbers to reflect that re-baselining means 35% equates to current mint rate. Open question: are we comfortable settling at 20% now that this will compound on itself?

we will rework to make self-consistent. I think the number gets reworked to around 25% down to 15% in the latter option. Let us put our heads together and then revise